by Bob Shively, Enerdynamics President and Lead Facilitator

The U.S. has traditionally been a natural gas importer that depends on pipeline supplies from Canada, and, to a lesser extent, amounts of gas via LNG tanker.

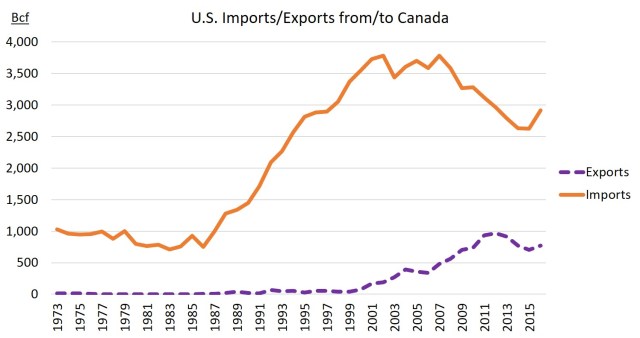

Source: Data from EIA website

But in recent years the shale gas boom has resulted in increasing pipeline flows into Mexico and Canada, and, beginning late last year, growth in LNG exports. As of mid-2017, the EIA projects that the U.S. will become a net exporter of natural gas.

Source: EIA Short-term Energy Outlook, August 2017

Net Exports Are Expected to Grow in Three Ways

This fundamental shift is expected to intensify in the coming years:

- Pipeline imports from Canada are expected to continually decline as lower-priced gas supplies from the Appalachian Basin continue to displace use of Canadian supplies in the Midwest and Northeast. Meanwhile exports are expected to continually grow into eastern Canada as U.S. supplies can undercut pricing from Western Canada.

Source: Data from EIA website - Pipeline imports to Mexico are growing rapidly along with growing construction of cross-border pipelines into Mexico.

Source: Data from EIA websitePipeline capacity into Mexico, which has grown more than threefold since 2010, is expected to again almost double by 2019.

- As LNG export projects currently under construction come online, LNG exports are expected to grow significantly.

Source: EIA Short-term Energy Outlook, August 2017

The EIA Short-term Energy Outlook for August 2017 forecasts 2018 exports of almost 4,000 Bcf. To give you a sense of magnitude, this equals more than 80% of forecast residential demand or almost 50% of industrial demand. So, there is no doubt that exports are becoming significant.

Impacts on U.S Consumers Are Uncertain

Clearly the growth in exports will be a benefit to gas producers who will see markets expand. Classic economics tell us that as demand grows, prices must increase. But interestingly, given the current belief in robust gas supplies, the forward gas price does not reflect such an expectation:

NYMEX natural gas futures prices as of August 10, 2017

Studies on the pricing impact of exports are varied. A 2015 study performed for the U.S. Department of Energy concluded that “in every case, greater LNG exports raise domestic prices and lower prices internationally.”[1] But a 2012 NERA study suggested that the increases would be small due to market factors:

“Natural gas price changes attributable to LNG exports remain in a relatively narrow range across the entire range of scenarios. Natural gas price increases at the time LNG exports could begin range from zero to $0.33 (2010$/Mcf). The largest price increases that would be observed after 5 more years of potentially growing exports could range from $0.22 to $1.11 (2010$/Mcf).”[2]

Industrial consumers in the U.S. are not convinced. The Industrial Energy Consumers of America (IECA) group recently sent a letter to Secretary of Energy Rick Perry expressing concerns that growing exports will negatively impact U.S. manufacturing. Others have suggested that while overall price levels may not go up much, price volatility will grow significantly, thus subjecting U.S. consumers to severe price risk.

Many factors will impact future prices of gas including growth of gas-fired power generation (perhaps following by declines in use for power generation if renewables continue to grow), growth in industrial demand, levels of exports, amounts of domestic production, and global natural gas price levels. After many years of historically low natural gas prices in the U.S., we must carefully watch developments in the coming years.

Footnotes

[1] U.S. DOE, The Macroeconomic Impact of Increasing U.S. LNG Exports, p. 8, available at https://energy.gov/sites/prod/files/2015/12/f27/20151113_macro_impact_of_lng_exports_0.pdf

[2] NERA Economic Consulting, Macroeconomic Impacts of LNG Exports from the United States, p. 2, available at https://energy.gov/sites/prod/files/2013/04/f0/nera_lng_report.pdf