by Bob Shively, Enerdynamics President and Lead Facilitator

For U.S. and Canadian natural gas markets, the 1990s were a fun time. Gas demand grew as independent power producers (IPPs) and utilities built new combined-cycle gas-fired generation and industrial customers took advantage of new lower-cost gas supplies. Regulators forced the break-up of vertical integration driven by long-term contracts between producers, pipelines, and utilities.

Opportunities for marketers blossomed as pipelines were forced to become open-access transport providers, and large customers bypassed their local distribution companies to purchase supply directly from the market. Pipelines also benefited as new customers were willing to commit to firm capacity to access supplies, leading to a boom in construction of pipeline projects.

Fast-forward 20 years: Today, Mexico is embarking on a similar path that promises to bring robust opportunities brought by growing demand, implementation of open-access pipeline rules, pipeline expansion projects, and opportunities for gas marketers.

In 2013, we wrote in a blog post that while Mexico may be a long-term large gas producer, it is was in the short-term on its way to being a robust export market for U.S. gas supply. This still holds true today, and the Mexican government and key gas users are taking critical steps to make market opportunities rapidly expand.

Natural Gas Supply and Demand

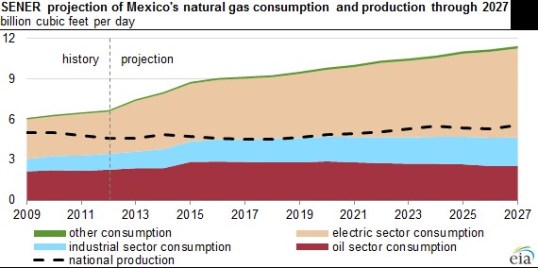

Demand for natural gas in Mexico has grown substantially in recent years driven by increasing use in industry and petroleum refining coupled with significant construction of new gas-fired electric generation. Growth is expected to continue throughout the next decade as shown in the following graph of demand projections from the Mexican energy ministry, SENER.

Source: http://www.eia.gov/todayinenergy/detail.cfm?id=16471

Much of the growth will be driven by the ongoing switch from oil to gas-fired generation with over 20 GW of new gas generation expected to be built by IPPs and the state-run electric utility CFE over the next five years[1].

While demand has grown, domestic gas production has declined as producers have focused more on oil production. Oddly for a country with the plentiful gas resources of Mexico, the result has been a need to increase imports both from U.S. pipelines as well as from LNG.

Use of imported gas is expected to continue to grow, driven by increasing imports from the U.S.

Pipeline Infrastructure

Historically, pipelines in Mexico were owned and operated by the national oil company PEMEX. The natural gas transport system was designed to serve southern loads from Mexican production in the Gulf of Mexico and northern loads via import pipelines from the U.S. LNG import capability was added in the late 2000s to supplement existing sources of supply on the southern system and to create new supply in northern Baja California. In recent years construction of additional import pipelines from the U.S. has exploded with import capacity doubling. Additional construction will continue as shown on the SENER graph above.

Market Restructuring and the Future

Perhaps the best news for interested market participants is that Mexico is rapidly implementing restructuring to open the markets to multiple parties. PEMEX’s monopoly on gas pipelines and sales has been ended by government fiat. The federal gas regulator, Comisión Reguladora de Energía (CRE), has been tasked with overseeing a transparent, impartial gas market. Rather than transferring ownership of the existing PEMEX pipelines, an independent gas system operator known as Centro Nacional de Control del Gas Natural (Cenegas) has been created to manage unbiased open access to pipeline capacity allowing use by gas marketers and even large end users.

Meanwhile, third parties are now allowed to build new pipelines. The electric utility CFE has been very active contracting for new pipelines. But often, all the space in new lines will not be used by CFE, thus opening capacity for other parties as well. Mexico hopes the result will be growth of a vibrant gas market with multiple participants entering the market. Given these expectations, there is talk of creating one or more price points within Mexico such as Monterrey or Reynosa (currently much of the gas in Mexico is priced as a basis to U.S. indices such as the Houston Ship Channel).

Given these developments, it appears Mexico is poised to enter a common competitive gas market with the U.S. and Canada. And there is even talk in the future of expanding pipelines into Central America to create a true uniform North American gas market. But of course, “the proof will be in the pudding” as they say, and we will eagerly watch to see how market developments play out.

Footnotes:

[1] Platts, Mexican Gas Market available at http://www.platts.com/IM.Platts.Content/Downloads/PDFs/mexican-gas-market.pdf

Pingback: Mexico’s Electricity Market Reforms Create New Opportunities | Enerdynamics