by Matthew Rose, Enerdynamics Instructor

The electric industry has long been blessed with electricity demand growth. Starting back in the 1950s, the industry benefited from the growing penetration of electric technologies  such as air conditioning and various appliances. The commercial market for electricity also grew due to the increased number of shopping centers and malls that required air-conditioned space and lighting. The electric utilities had their mandate: make sure there was enough power to keep up with demand.

such as air conditioning and various appliances. The commercial market for electricity also grew due to the increased number of shopping centers and malls that required air-conditioned space and lighting. The electric utilities had their mandate: make sure there was enough power to keep up with demand.

Some 50 years later, the question is “what happens now?” Demand is barely growing with some companies even seeing a forecasted loss in their demand requirements. How do utilities remain viable, competitive businesses attracting investors with demand shrinking? The end result is a needed examination of the way the industry is regulated and compensated while allowing companies the ability to map out a sustainable and meaningful future.

Evidence of the situation

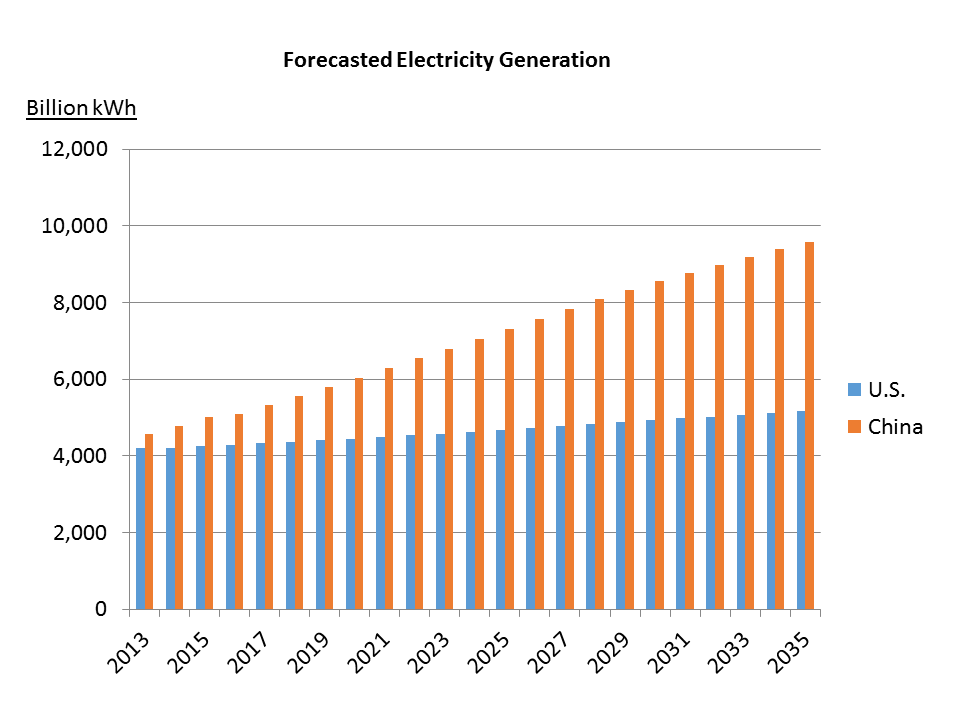

There are a number of possible explanations for the notable drop in electricity demand. While the factors behind the trend seem varied, demand requirements across the country have steadily declined over recent decades. Although there are exceptions with some utilities still experiencing notable demand growth, the overall trend shows a stark reality for most electric utilities:  Source: Energy Information Administration as presented in paper by F. Sioshansi. Why the Time has come to Rethink the Electric Business Model. The Electricity Journal, August/September 2012.

Source: Energy Information Administration as presented in paper by F. Sioshansi. Why the Time has come to Rethink the Electric Business Model. The Electricity Journal, August/September 2012.

Reasons behind this decline are varied, inter-related, and wide-ranging. For some companies, customer growth has simply stagnated, and loss of a large industrial customer load has impacted demand. For others there are notable, longer-term drivers directly impacting customer demand.

Key drivers impacting demand requirements

Key factors driving the decline in customer demand include the impact of emerging technology advancements and policy directives at both the federal and state levels. Although these are not the sole contributors, these considerations result in notable changes in the utility-customer relationship. The key considerations include:

- growth in distributed generation and renewable assets

- expanded state directives advancing energy efficiency

- the impact of federal and state building codes and equipment standards

- robust demand response markets

These drivers differ from other issues that traditionally impacted utility operations such as extended weather and temperature patterns, uncertain energy usage patterns of large customers, or the overall health of the economy – issues that tend to be of shorter duration and offer opportunities for risk management. In contrast, the above-noted drivers reflect fundamental changes over the long term, including shifting the production and management of electricity to consumers.

A more detailed discussion of the above-mentioned key drivers is available in our Q2 issue of Energy Insider.

Next week’s post will continue this discussion and will focus on the implications and future risks and challenges that utilities face in years to come.

References

1. Navigant Research, Distributed Solar Energy Generation. April 2013.

2. American Council for Energy Efficient Economy, Three Decades and Counting: A Historical Review and Current Assessment of Electric Utility Energy Efficiency Activity in the States. June 27, 2012.

3. Lawrence Berkeley Laboratory, The Future of Utility Customer-Funded Energy Efficiency Programs in the United States: Projected Spending and Savings to 2025. January 2013.

4. EnerNOC Utility Solutions Consulting, Factors Affecting Electricity Consumption in the U.S. (2010-2035). March 2013.

5. FERC, 2012 Demand Response and Advanced Metering Survey. December 2012.

Related articles

- Will Demand Response, Distributed Energy Bring End of Traditional Utility Business Model? (theenergycollective.com)

generation capacity quickly. My team’s job was to find good candidates for installing cogeneration[1] and demonstrate to the customer the economics associated with making the investment.

generation capacity quickly. My team’s job was to find good candidates for installing cogeneration[1] and demonstrate to the customer the economics associated with making the investment.