by Bob Shively, Enerdynamics President and CEO

“..the process of setting an allowed ROE has consistently proven to be the most contentious and subjective part of a rate case proceeding.”[1]

Much of the key natural gas and electricity infrastructure in the U.S. operates under the cost-of-service ratemaking. This is true for electric  transmission and distribution, gas distribution, and most gas transmission lines. Cost-of-service ratemaking sets rates based on forecasted costs of providing service plus a “reasonable” rate of return on the equity invested by shareholders to build the capital facilities necessary to provide service. The return on equity (ROE) authorized by the regulator is not guaranteed since business results such as expenses and sales often impact the true return. Still, the authorized ROE is a key component of the expected level of earnings for a regulated utility.

transmission and distribution, gas distribution, and most gas transmission lines. Cost-of-service ratemaking sets rates based on forecasted costs of providing service plus a “reasonable” rate of return on the equity invested by shareholders to build the capital facilities necessary to provide service. The return on equity (ROE) authorized by the regulator is not guaranteed since business results such as expenses and sales often impact the true return. Still, the authorized ROE is a key component of the expected level of earnings for a regulated utility.

Under ratemaking theory, the authorized return should balance the interests of ratepayers and shareholders: The rate should be just high enough to attract needed capital to maintain service reliability but no higher since anything above that level would provide shareholders with a profit level above what is necessary.

Rates of return are set by regulators after testimony by interested parties and analysis by regulatory staff. They vary based on the return on alternate investments such as bonds and other conservative business option, the amount of capital required, perceived risk associated with a specific company, and the regulatory climate in a specific locale.

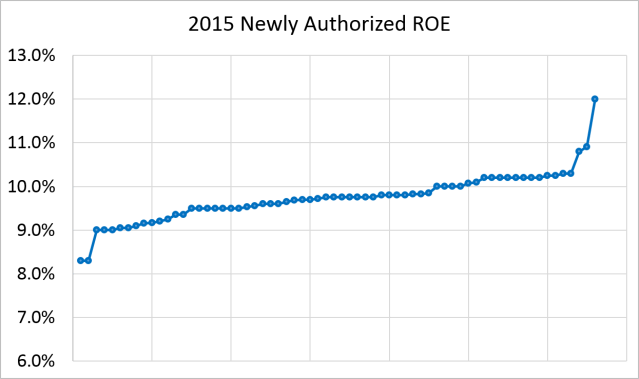

Public Utilities Fortnightly has annually surveyed ROE authorized by state commissions since 1982. This year, authorized returns in the survey ranged from a low of 8.3% (ATCO electric and ATCO gas) to a high of 12.0% (Lockhart Power Company). As shown in the graph below, most decisions clustered in the range of 9.0 to 10.3%.

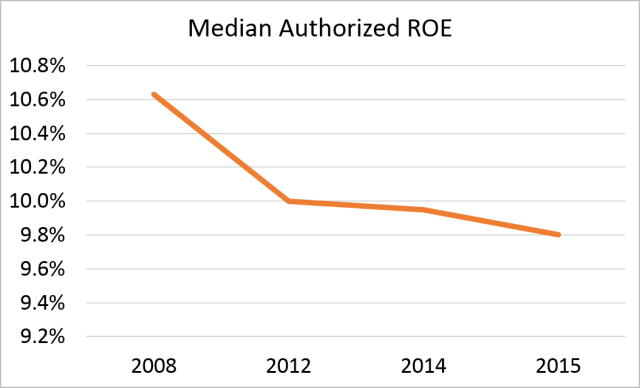

In 2015, the median ROE was 9.8%. Since the economic downturn in 2008, ROE have dropped significantly as interest rates have fallen and investors have looked for lower risk inherent in most utility investment.

Given the size of many utilities’ ratebases, a small change in ROE can result in a change of authorized earnings of many millions of dollars. And, of course, the flip side to that is that a small change can result in a change of rate levels paid by consumers.

So the next time your company goes in for a cost-of-capital case, you’ll realize just how much is riding on the percentage authorized by the regulator. And using the information from the Public Utilities Fortnightly annual study, you’ll be able to see how your company stacks up compared to other utilities.

Footnotes:

[1] “Equity Returns: ‘Allowed’ vs. Earned”, Phillip S. Cross, Public Utilities Fortnightly, November 2015

these key global problems. The swords that cut this Gordian Knot: breakthrough technologies built and deployed by entrepreneurial companies with global scope.” ~ Reid Hoffman, LinkedIn founder[1]

these key global problems. The swords that cut this Gordian Knot: breakthrough technologies built and deployed by entrepreneurial companies with global scope.” ~ Reid Hoffman, LinkedIn founder[1]

costs fluctuate so much. Some say it is due to market control by generation owners who

costs fluctuate so much. Some say it is due to market control by generation owners who

Russia, we wrote

Russia, we wrote