by Bob Shively, Enerdynamics President and Lead Instructor

Despite low prices and falling drilling rates, natural gas production is expected to grow more in 2016 due to increased drilling efficiency, price-hedged production, and producers who either physically or financially can’t stop producing quickly.

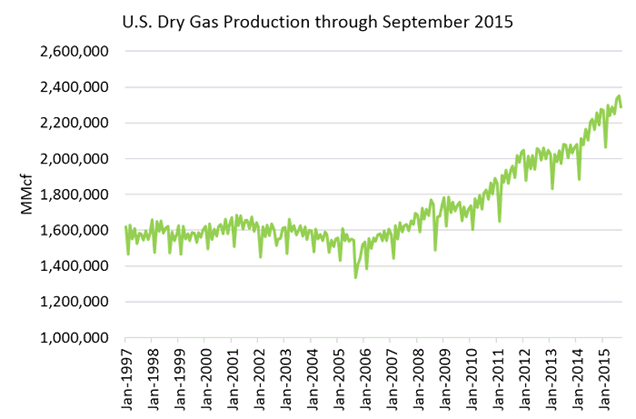

The Energy Information Administration (EIA) forecasts that annual production in 2016 will increase by almost 2% over 2015 levels, adding additional production of over 500 Bcf.

source: www.eia.gov

Unprecedented supply led to prices in December 2015 that were the lowest seen in any month since 1998. So much for the winter price boost that producers used to count on!

So how will high supply and low prices impact the gas business in 2016? Here are a few of my predictions:

1. There will be some demand growth but maybe not as much as would be expected given such low prices

Most forecasts for 2016 demand suggest that levels will be similar to 2015 with increases less than one-half a percent. Why is there little demand growth given the falling prices? Most forecasts predict a warm winter in the critical heating markets of the Midwest and Northeast, thus pushing residential and commercial demand levels lower. But we may see an increase in industrial demand given new chemical and fertilizer projects coming online.

Projections for power consumption are mixed. Natural gas generation output has already passed coal output for the first time in U.S. energy history, and some believe that any price-based fuel switching has already occurred. We believe a bit more price switching will still occur and there will certainly be more coal retirements in 2016 to help gas generation grow. But other factors will hold down the growth rate. Rapidly growing renewable generation tends to displace gas generation, and and the overall growth of electric demand is relatively flat. So while there is a little room for generation demand growth, it appears it will be modest. At most, demand may grow by less than 40% of the expected growth in production.

2. Exports will help some but may not be significant enough to change the supply/demand equation

Exports of natural gas are growing. In 2016 we will see the first major LNG exports from the U.S. with the commissioning of the Cheniere Sabine Pass terminal. Alaska has exported small amounts of LNG for many years. Receiving much less attention is the growth of pipeline exports to Mexico. Despite significant gas reserves in Mexico, a growing gas market cannot wait for industry reform to increase production of these reserves. Instead existing pipelines are carrying gas south from the U.S., and new pipeline projects will provide additional U.S. to Mexico capacity.[1] Unfortunately growing LNG and Mexico exports, like domestic demand, may soak up a portion of the excess supply but will not be sufficient to dramatically change the supply/demand equation.

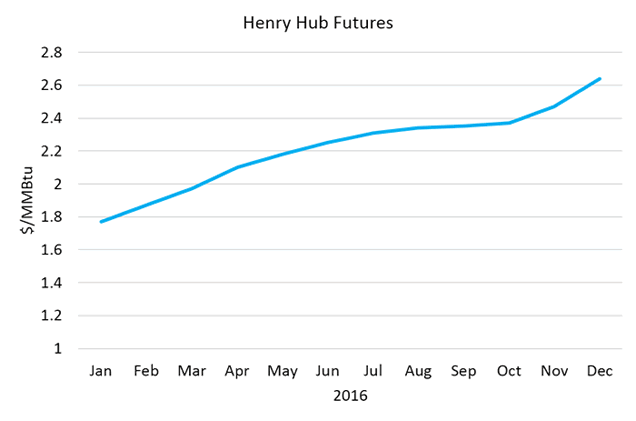

3. Given supply and demand, low prices are expected to last throughout 2016

The forward price curve for 2016 does not indicate an increase in prices. In fact, you have to go to January 2018 to find a futures price higher than $3.00/MMBtu and to January 2025 to find one higher than $4.00/MMBtu!

source: www.cmegroup.com

source: www.cmegroup.com

Certainly drilling will continue its decline. Current rig counts are 25% what they were just four years ago. But producers are somewhat of a victim of their own success as they have increased production per well by such an extent that fewer rigs does not reduce supply as much as one might expect.

So what will 2016 look like?

First, while many seem to focus on doom and gloom for producers, the current situation is a huge boom for many including gas customers and workers in certain industries. Some examples of the upside include:

- Residents will heat their homes this winter for as little as half what they were paying just a few years ago.

- Major industrial manufacturers are shifting production back to the U.S. and making long-term investments here based on low gas prices.

- In the electric industry, low gas prices have allowed the U.S. to begin cutting greenhouse gas emissions with a low threshold of economic pain.

- Supply ready for European export provides geopolitical benefits as our European allies are no longer tied to supply from Russia.

- For the producers that survive low prices, a solid long-term market is being locked in now.

I have been in the gas industry long enough to witness three boom-bust cycles. Each time, many preached that we had a “new normal” situation and that the industry should accept that the history of cycles is no longer valid. In each instance when everyone thought we had a new normal, we suddenly didn’t, and a new cycle began. Just remember that at some point, this cycle too shall pass.

Footnotes:

[1] See for instance: http://bv.com/energy-strategies-report/april-2015-issue/fuels-focus-growing-natural-gas-opportunities-in-mexico