by Bob Shively, Enerdynamics President and Lead Instructor

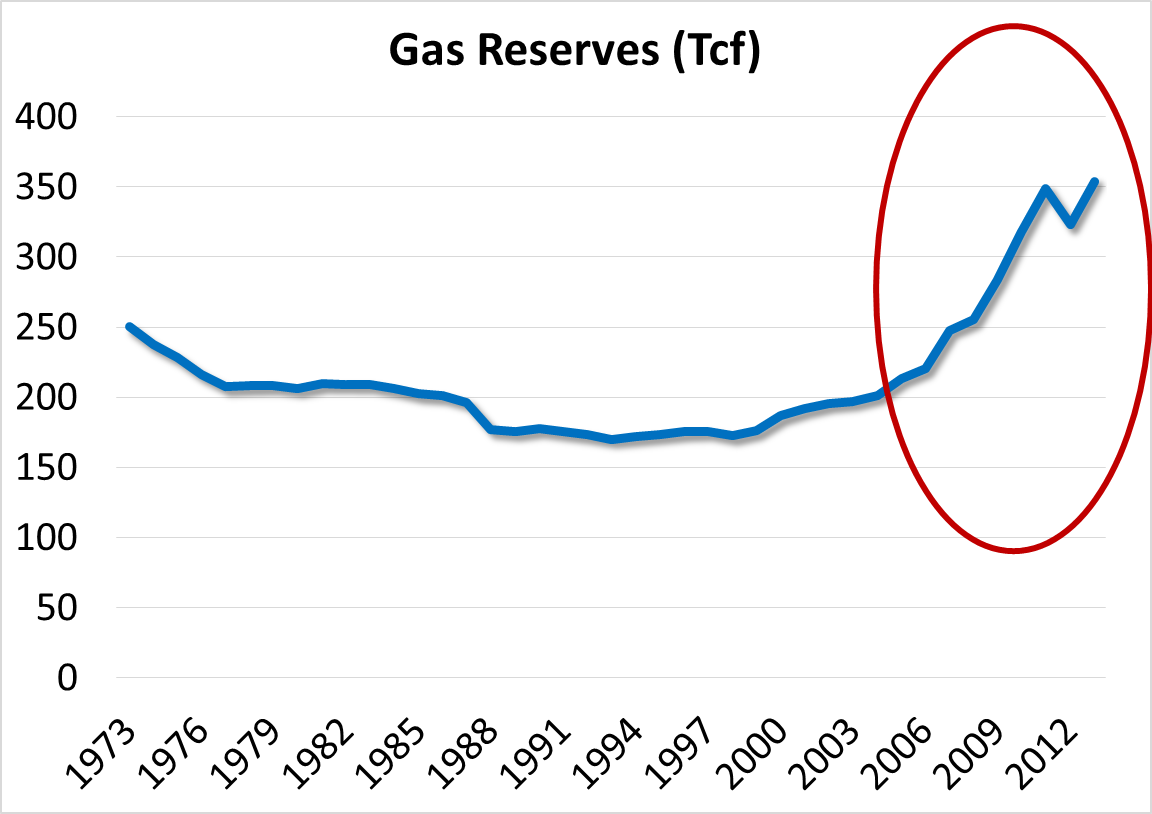

They say a picture, or in this case a graph, is worth a thousand words. Take a look at the change in U.S. natural gas reserves:

Source: EIA.gov

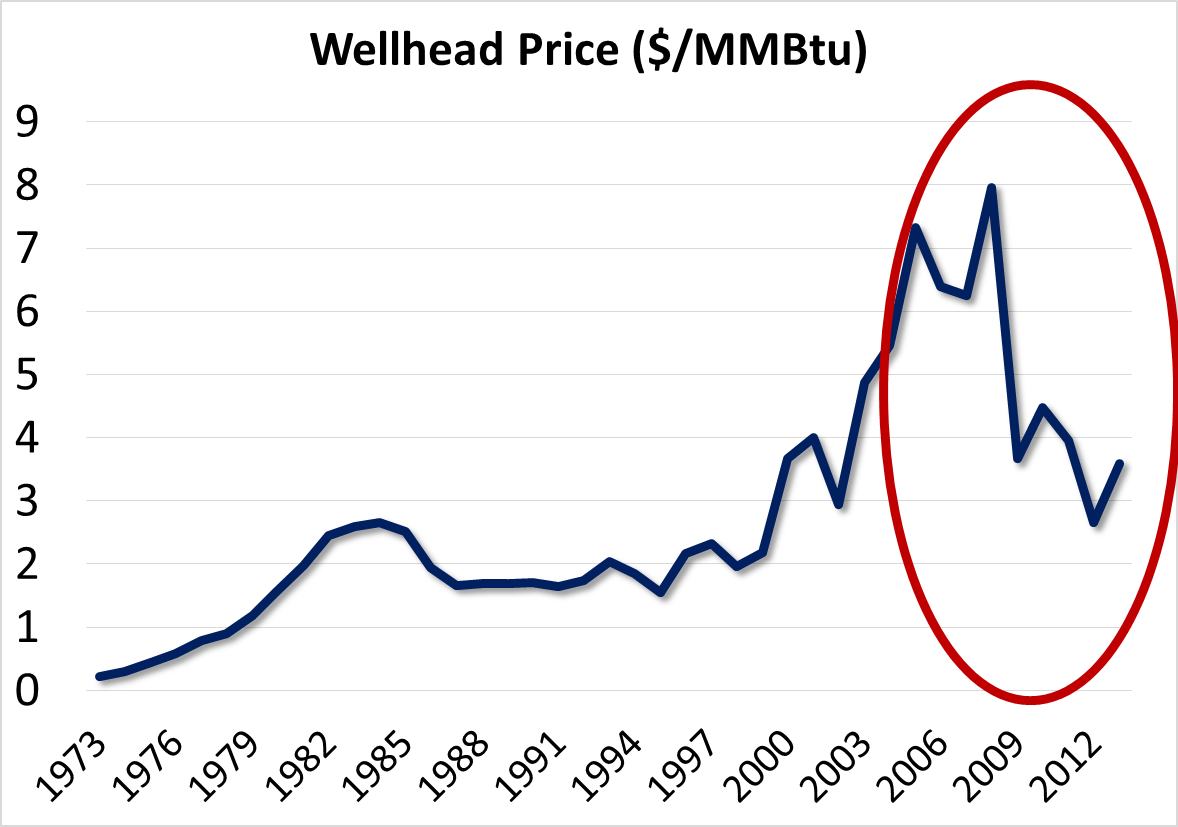

Source: EIA.gov

Without looking at it, it is hard to imagine the flabbergasting growth in U.S. natural gas reserves in the last five years. And, even more amazing, this growth has occurred in a time of falling prices.

Source: EIA.gov

It’s common industry knowledge that this situation is a result of the dramatic impact of shale gas resource development driven by new hydraulic fracturing (a.k.a. fracking) techniques. This has created significant benefit for consumers of natural gas and electricity as lower gas prices have driven down electric generation costs.

So can the party continue? Or will the seemingly inevitable bust hit the markets? Let’s consider a few fundamental factors:

1. Will demand grow enough to suck up the excess supply resulting in price increases?Growing power plant demand seems certain, and, with a number of large industrial facilities under construction, growing industrial demand also seems likely. And liquefied natural gas (LNG) exports will soon become reality. This could be enough to change the supply/demand balance. Here is the current Energy Information Administration (EIA) forecast for U.S. natural gas demand net of imports/exports:

This shows steadily increasing demand over time, which, if the forecast is correct, suggests that prices should rise. But there is nothing here to show demand growing with anywhere near the dramatic increase we have seen in reserves. So while this might move prices up a bit, it seems it should not result in huge price increases like we saw in the mid to late 2000s.

2. Can producers restrict production by reducing drilling (i.e. leave reserves in the ground) thus causing prices to rise? To address this question, look at this graph from the EIA website that plots the monthly number of natural gas rigs in operation:

We see a graph that should look hopeful for producers seeking higher prices since the number of rigs has fallen significantly. But then we realize that gas is often found in conjunction with oil and the number of oil rigs has increased dramatically:

And the fact remains that most producers need cash flow, so there is only so much they can do to restrict supply.

Given these facts, it is hard to see the party for gas consumers ending at least in the near-term. But, as we all know, the gas industry has been boom-bust for many years, and there may be unexpected twists lying in wait.